Thursday, November 29, 2012

Sunday, November 25, 2012

25 surprising facts about the increasingly mobile nature of online and in-store retail - Quartz

25 surprising facts about the increasingly mobile nature of online and in-store retail - Quartz

132% more money was spent by UK marketers on mobile advertisements in 2012 than 2011

88% of ecommerce in the world is still conducted on PCs; in the US, that figure is 81%

Thursday, November 22, 2012

The HP/Autonomy Kerfuffle: Why Due Diligence Doesn't Matter

HP should have known all about Autonomy - FT.com

I find this HP/Autonomy $8B write down fascinating. How can a large company like HP lack the resources to execute thorough due diligence? HP hired "blue chip" accounting firms like KPMG to conduct due diligence. You would assume that blue chip i/banks and accounting firms would be able to uncover egregious shenanigans hidden in a target company. Apparently, it doesn't matter.

1. Deferred Revenue: From my experience in telecommunications, there are NUMEROUS ways to fabricate, inflate, extract, derive, book, include, communicate or accept revenue. I've seen many directors and sales personnel book revenues from all sorts of angles, in an effort to meet quota, or even worse, YEAR END goals. The only way to drill down actual sales, is to monitor churn rates from lines of businesses. Good luck with that.

2. Due Diligence: Due diligence doesn't really mean anything. For i/bankers it means make sure you make it easy for the acquirer to sleep at night pre-acquisition. For accountants it means, make it easy for the acquiring company to use audited financials for securing financing for the acquisition. For the acquiring company it means make it easy for our board of directors and shareholders to justify our rationale for acquiring the target company (and increase our bonuses! :) ).

3. Post-Acquisition Integration: Most mergers and acquisitions erode shareholder value for one main reason: company culture. Company culture is synonymous with individual personalities. Marriages fail mostly for the same issues - lack of compatibility. In HP's case, they should have kept Autonomy as a standalone entity, and kept Autonomy's managers as-is, with a bulk of the purchase price in an earn-out. Earn-outs are crucial for techie companies because of the issue with revenue recognition.

I really can't blame Autonomy for this debacle. In my opinion, HP is to blame, mainly due to their decision to integrate and their addiction to growth via acquisition. Growth by acquisition can work if the acquiring company is growing organically and is seeking to increase their market share WITHIN their industry. It can work if a company is seeking to defend their position or to enter a new market. It doesn't work if a company isn't growing organically or if a company depends on it solely for top line purposes.

I find this HP/Autonomy $8B write down fascinating. How can a large company like HP lack the resources to execute thorough due diligence? HP hired "blue chip" accounting firms like KPMG to conduct due diligence. You would assume that blue chip i/banks and accounting firms would be able to uncover egregious shenanigans hidden in a target company. Apparently, it doesn't matter.

1. Deferred Revenue: From my experience in telecommunications, there are NUMEROUS ways to fabricate, inflate, extract, derive, book, include, communicate or accept revenue. I've seen many directors and sales personnel book revenues from all sorts of angles, in an effort to meet quota, or even worse, YEAR END goals. The only way to drill down actual sales, is to monitor churn rates from lines of businesses. Good luck with that.

2. Due Diligence: Due diligence doesn't really mean anything. For i/bankers it means make sure you make it easy for the acquirer to sleep at night pre-acquisition. For accountants it means, make it easy for the acquiring company to use audited financials for securing financing for the acquisition. For the acquiring company it means make it easy for our board of directors and shareholders to justify our rationale for acquiring the target company (and increase our bonuses! :) ).

3. Post-Acquisition Integration: Most mergers and acquisitions erode shareholder value for one main reason: company culture. Company culture is synonymous with individual personalities. Marriages fail mostly for the same issues - lack of compatibility. In HP's case, they should have kept Autonomy as a standalone entity, and kept Autonomy's managers as-is, with a bulk of the purchase price in an earn-out. Earn-outs are crucial for techie companies because of the issue with revenue recognition.

I really can't blame Autonomy for this debacle. In my opinion, HP is to blame, mainly due to their decision to integrate and their addiction to growth via acquisition. Growth by acquisition can work if the acquiring company is growing organically and is seeking to increase their market share WITHIN their industry. It can work if a company is seeking to defend their position or to enter a new market. It doesn't work if a company isn't growing organically or if a company depends on it solely for top line purposes.

Tuesday, November 20, 2012

Friday, November 16, 2012

Hostess Brands Files Bankruptcy

There are 12 different unions, with some 15,000 members, 40 separate pension plans, and $2 billion in unfunded pension liabilities. (Whew!) That's what Hostess claims is at the heart of the company's woes. The unions say management was fine with those pensions after the first bankruptcy and may go on strike if they feel they're being made the fall guys in any court-ordered restructuring. That would be the end of Hostess as we know it.

THE PE FIRM

Run by Tim Collins, a financier with Democratic Party connections, private equity firm Ripplewood Holdings acquired control of Hostess as it came out of its first bankruptcy in 2009. Ripplewood pumped a total of $170 million into the company, but the string of CEOs it appointed could not keep Hostess from sliding back into Chapter 11 (cheekily called Chapter 22 in some circles). While it still retains some debt, Ripplewood has little chance of recouping any of its investment.

THE HEDGE FUNDS

Silver Point Capital and Monarch Alternative Capital, hedge funds that specialize in distressed companies, are both said to hold about 30% of Hostess's debt. Sources say their current stake is between $50 million and $100 million apiece, though they originally invested more. The goal now: renegotiate the Teamsters' contract and get out as soon as possible. Or liquidate the company and just take what they can get. As the holders of Hostess's senior secured debt, either way the hedgies will walk away with plenty.

CAKE WRECK: HOSTESS FROM ICON TO BUST

- 1925: Continental Baking Co. buys Taggart Baking, maker of Wonder Bread. Continental becomes the largest bakery in the U.S.

- 1930: Continental baker James Dewar gets the idea to make an inexpensive cream-filled sponge cake using strawberry shortcake equipment that sat idle in the off-season. The Twinkie is born.

- 1930: Wonder Bread becomes the first large-scale baker to sell loaves of presliced bread. The company's advertising is thought to be the origin of the phrase "the greatest thing since sliced bread."

- 1947: Mascot Twinkie the Kid is introduced.

- 1947: Hostess introduces white Sno Balls. It takes about three years for the company to add the cream filling and distinctive pink color.

- 1950s: Hostess Twinkies sponsors The Howdy Doody Show, reinforcing its status as a ubiquitous lunchbox treat.

- 1967: Hostess introduces Ding Dongs and Ho Hos.

- 1979: "Twinkie defense" is coined during the trial of Dan White, who binged on junk food before killing San Francisco's mayor and city supervisor Harvey Milk.

- 1992: Seinfeld's Newman reveals a passion for Drake's Coffee Cake, now part of Hostess Brands.

- 1995: Interstate Bakeries Corp. acquires Continental, the country's largest wholesale baker, for $220 million in cash plus stock. Interstate becomes the nation's largest bakery company.

- 1999: Hillary Clinton approves the inclusion of Twinkies in the Millennium Time Capsule, alongside Ray Charles' sunglasses and a piece of the Berlin Wall. The Twinkies are removed, however, because of rodent concerns.

- 2004: Citing pressure from carb-conscious consumers, rising ingredient costs, and climbing expenses for employee pensions and health care, Interstate Bakeries files for Chapter 11.

- 2009: Woody Harrelson risks his life in an obsessive search for Twinkies in the post-apocalyptic hit Zombieland.

- 2009: Backed by private equity, the company exits bankruptcy as a private entity and changes its name to Hostess Brands.

- 2012: Hostess again enters bankruptcy, this time with 19,000 employees and $860 million in debt

Wednesday, November 14, 2012

{kind=link}

The Rise of the Social Entrepreneur

The Rise of the Social Entrepreneur - NYTimes.com interesting article from New York Times

In my opinion, there's no reason for anyone to NOT start a business, if you're interested. The costs associated with starting a business are almost down to zero. Need a web site? Wix.com. Need incorporation and business documents? Legalzoom.com. Need a server? Amazon.com. Need marketing? Facebook, Twitter, Instagram and even Linked In. Need professional number? Grasshopper.com. Need a swanky office address and part time office space? Try regus.com.

What prevents people from launching a business is perspective, fear and lack of drive. Desperation can fuel success. Or at least motivation. When I meet entrepreneurs with amazing and sometimes ludicrous ideas, I never discourage them. Why? Why should I? The market (and timing) determines success.

I view entrepreneurship as a casino: You'll never win if you don't play. With the current "new normal" economy, coffee shops are filled with freelancers and cash flow positive businesses. From my time in Boston and recently Austin, the new normal is alive and kicking. From food trucks to dog walking, to personal assistants, to software services, there's no longer any reason NOT to start a business....

In my opinion, there's no reason for anyone to NOT start a business, if you're interested. The costs associated with starting a business are almost down to zero. Need a web site? Wix.com. Need incorporation and business documents? Legalzoom.com. Need a server? Amazon.com. Need marketing? Facebook, Twitter, Instagram and even Linked In. Need professional number? Grasshopper.com. Need a swanky office address and part time office space? Try regus.com.

What prevents people from launching a business is perspective, fear and lack of drive. Desperation can fuel success. Or at least motivation. When I meet entrepreneurs with amazing and sometimes ludicrous ideas, I never discourage them. Why? Why should I? The market (and timing) determines success.

I view entrepreneurship as a casino: You'll never win if you don't play. With the current "new normal" economy, coffee shops are filled with freelancers and cash flow positive businesses. From my time in Boston and recently Austin, the new normal is alive and kicking. From food trucks to dog walking, to personal assistants, to software services, there's no longer any reason NOT to start a business....

Tuesday, November 13, 2012

LBO Shenanigans pt 1

As I mentioned previously, I'm a fundless sponsor. It means that I raise capital for acquisitions on a deal by deal basis. I have loosely committed capital from equity and leverage sources. The upside to this method of investing in businesses is that I do not have any pressure to make investments. Also, I can make investments based specific investor criteria.

An interesting phenomenon within the past three years, is that middle-market CEO's initially wanted too much for their company. They were looking to extract as much value from their companies as humanly possible, thereby indirectly guaranteeing bankruptcy or default, post acquisition.

NOW? CEO's have been brought down to reality. Why?

1. Sponsors are weary of the market. Companies have flat top line growth. Cutting costs can only do so much for earnings. Unless a target company has a ridiculous amount of sales backlog, it will be difficult to prove that your company is growing.

2. Low interest rates have artificially inflated asset values, and simultaneously driven down equity risk premia.

3. The Facebook Effect: The recent FB IPO debacle proves the point. Most companies are overvalued. Other examples include Zynga, Groupon, etc.

SOLUTIONS?

1. Sellers should be more willing to meet buyers more than halfway. If CEO's actually believe that their company is worth X + 30%, they should be willing to reinvest or defer compensation over a number of years.

2. Buyers should take advantage of low interest rates. I've seen middle market companies borrow at sub 3% rates. In such a case, buyers can become creative when structuring acquisitions. A mix of reverse PO financing, vendor financing, mezzanine, hard money and SELLER financing should do the trick. With more leverage, you can offer sellers a significant premium to close immediately.

With M&A activity down more than 18% YoY, I wonder if everyone has cold feet, or if there's something else coming around the corner. Either way, there are a lot of opportunities in this market place, and I intend on taking advantage of it before the party is over.

An interesting phenomenon within the past three years, is that middle-market CEO's initially wanted too much for their company. They were looking to extract as much value from their companies as humanly possible, thereby indirectly guaranteeing bankruptcy or default, post acquisition.

NOW? CEO's have been brought down to reality. Why?

1. Sponsors are weary of the market. Companies have flat top line growth. Cutting costs can only do so much for earnings. Unless a target company has a ridiculous amount of sales backlog, it will be difficult to prove that your company is growing.

2. Low interest rates have artificially inflated asset values, and simultaneously driven down equity risk premia.

3. The Facebook Effect: The recent FB IPO debacle proves the point. Most companies are overvalued. Other examples include Zynga, Groupon, etc.

SOLUTIONS?

1. Sellers should be more willing to meet buyers more than halfway. If CEO's actually believe that their company is worth X + 30%, they should be willing to reinvest or defer compensation over a number of years.

2. Buyers should take advantage of low interest rates. I've seen middle market companies borrow at sub 3% rates. In such a case, buyers can become creative when structuring acquisitions. A mix of reverse PO financing, vendor financing, mezzanine, hard money and SELLER financing should do the trick. With more leverage, you can offer sellers a significant premium to close immediately.

With M&A activity down more than 18% YoY, I wonder if everyone has cold feet, or if there's something else coming around the corner. Either way, there are a lot of opportunities in this market place, and I intend on taking advantage of it before the party is over.

Monday, November 12, 2012

Hitting Bottom + Idea Sex: Altucher Confidential

Hitting Bottom, Idea Sex, How Not To Pay Student Loans, and More Altucher Confidential

The Entrepreneur Commandments, volume 1

The Entrepreneur Commandments, volume 1

Sunday, November 11, 2012

Buttonwood: Desperately seeking yield | The Economist

Buttonwood: Desperately seeking yield | The Economist

"For investors, the risks are twofold. The first is that economies will dip back into recession and that more companies will default on their bond issues, forcing investors to suffer write-downs on their holdings. The credit risk of corporate bonds is reflected in the excess interest rate, or spread, they offer over government bonds. At the moment this spread is lower than it was at the start of the year and lower than its five-year average. But it is still well above the levels of 2005 and 2006, when the credit bubble was inflating."

The thirst for yield continues. It's difficult not to invest in corporate bonds, with most yielding 5-6%. Even the trashiest companies are borrowing at record low yields. But when will the party end? Bernanke has committed to record low interest rates until 2015-ish. With stagnant global economic growth, I don't see money supply-induced inflation on the horizon. Price inflation doesn't count, since supply-side variables could spark a price increase in commodities.

So what's the case for equities? Equities are currently overvalued, in my opinion, since low interest rates have artificially increased asset/security values. M&A activity is curiously low. Companies would rather increase dividends, increase buybacks or just sit on cash at 0%.

In my opinion, investing in preferred stock appears to be the best bet. Whether as an investor, you're privy to preferred public equities, or if you invest in private equity (especially higher beta private companies), the rewards are tremendous, if you do stay the course...

With a low VIX and low trading volumes, I wouldn't put my money in public stocks...However, caveat emptor...

"For investors, the risks are twofold. The first is that economies will dip back into recession and that more companies will default on their bond issues, forcing investors to suffer write-downs on their holdings. The credit risk of corporate bonds is reflected in the excess interest rate, or spread, they offer over government bonds. At the moment this spread is lower than it was at the start of the year and lower than its five-year average. But it is still well above the levels of 2005 and 2006, when the credit bubble was inflating."

The thirst for yield continues. It's difficult not to invest in corporate bonds, with most yielding 5-6%. Even the trashiest companies are borrowing at record low yields. But when will the party end? Bernanke has committed to record low interest rates until 2015-ish. With stagnant global economic growth, I don't see money supply-induced inflation on the horizon. Price inflation doesn't count, since supply-side variables could spark a price increase in commodities.

So what's the case for equities? Equities are currently overvalued, in my opinion, since low interest rates have artificially increased asset/security values. M&A activity is curiously low. Companies would rather increase dividends, increase buybacks or just sit on cash at 0%.

In my opinion, investing in preferred stock appears to be the best bet. Whether as an investor, you're privy to preferred public equities, or if you invest in private equity (especially higher beta private companies), the rewards are tremendous, if you do stay the course...

With a low VIX and low trading volumes, I wouldn't put my money in public stocks...However, caveat emptor...

Believe None of What You Hear + Half of What You See...

Close to a year ago, I stopped watching the news. By news I mean, MSNBC, CNN, Fox News, CNBC and local news. Why? There is nothing pertinent to learn or gather from watching the news. Pundits and "very serious people" use numbers, percentages and term du jour like "fiscal cliff", "uncertainty", debt/GDP and "austerity", to explain market economics. Well, all of it is nonsense.

- Macroeconomics: The stock market does not reflect the real economy. Just because S&P is up/down 500 points on Monday, doesn't mean that your local dry cleaning business will boom or bust the next day. It baffles me when "very serious people" explain that the reason why the S&P went down was because, "Investors are worried about the ECB..."; "Investors are worried about the fiscal cliff..."; "Investors are worried about the political instability in the state of Florida". The stock market is purely behavioral. If an investor comes to work the day after his wife tells him she's filing for divorce, that will obviously affect his investment decisions. If you watch CNBC Squawk Box and make investment decisions STRICTLY because a VSP said so, then you need help.

- Microeconomics: Companies make selfish decisions. In other words, companies make decisions regardless of what they should do in theory. Current low interest rates means that Federal Reserve wants companies to take risks. In theory, companies should borrow at 3%, invest in fixed assets, R&D, hire new people, spend money on glitzy marketing campaigns and/or buy competitors. Nope. What companies did was refinance existing debt. That's it. Why? Well, why should they? Why take any risks like HIRING new people, if you don't need new hires? Why invest in a $300M factory, if you don't need it? Those decisions have nothing to do with "fiscal cliff" or "uncertainty".

Companies are sitting on close to $3T in cash. Conceptually, they do not want to sit on cash because it's costing them money directly and indirectly. So what are they doing? Stock buybacks and dividends...Sheeeesh.

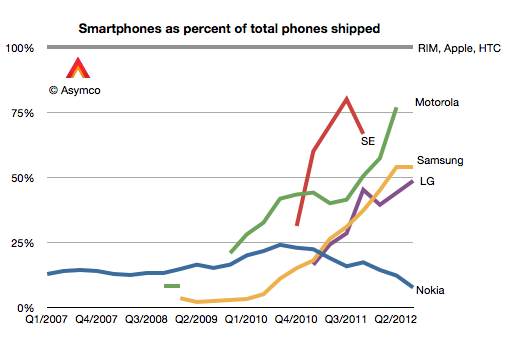

Why Only Samsung Builds Phones That Outsell iPhones - Businessweek

Why Only Samsung Builds Phones That Outsell iPhones - Businessweek

As a former wireless industry employee, I have always been an advocate for Samsung mobile devices (and previously Blackberry). They've always designed and manufactured elegant devices. They also had the first mobile phone + mp3 device pre-iPhone.

Samsung's only kerfuffle has been:

1. Incoherent Marketing Strategy

2. Lack of Brand Loyalty (think Sony)

But Samsung has impressed me lately. Unlike their competitors, RIM, Nokia and Motorola, who had clear advantages of taking over or aggressively competing with Apple, Samsung was quick enough to copy Apple's success, and has been rewarded with a formidable smartphone market share.

Taking their cue from Apple, Samsung quickly realized that copying is better than inventing. Why invent? Besides securing profitable patents and "first mover" fanfare, there aren't any more advantages for being first. Being first means others will learn or profit from your mistakes.

Samsung has the production scale and in-house infrastructure to compete with Apple aggressively. The Galaxy S's and Notes are just as good (if not better) than iPhone's and iPads. Samsung, and pretty much every company, lags behind Apple in terms of brand awareness and customer loyalty. Besides that, there are numerous advantages of being number two...or a late bloomer.

As a former wireless industry employee, I have always been an advocate for Samsung mobile devices (and previously Blackberry). They've always designed and manufactured elegant devices. They also had the first mobile phone + mp3 device pre-iPhone.

Samsung's only kerfuffle has been:

1. Incoherent Marketing Strategy

2. Lack of Brand Loyalty (think Sony)

But Samsung has impressed me lately. Unlike their competitors, RIM, Nokia and Motorola, who had clear advantages of taking over or aggressively competing with Apple, Samsung was quick enough to copy Apple's success, and has been rewarded with a formidable smartphone market share.

Taking their cue from Apple, Samsung quickly realized that copying is better than inventing. Why invent? Besides securing profitable patents and "first mover" fanfare, there aren't any more advantages for being first. Being first means others will learn or profit from your mistakes.

Samsung has the production scale and in-house infrastructure to compete with Apple aggressively. The Galaxy S's and Notes are just as good (if not better) than iPhone's and iPads. Samsung, and pretty much every company, lags behind Apple in terms of brand awareness and customer loyalty. Besides that, there are numerous advantages of being number two...or a late bloomer.

Wednesday, November 7, 2012

WTH does "Uncertainty" Mean?

Since when is life or business certain? As Mitt Romney's tax returns clearly demonstrated, not even taxes are certain. The "Very Serious People" who claim that the stagnant economy can be blamed on government-induced "uncertainty", are clearly misinformed, or passing the blame on every "job creators" favorite punching bag.

Based on my direct dealings with lower middle-market enterprises ($50 > enterprise value), the biggest problem affecting incremental increases in capex, is lack of demand. Companies do not need additional goods and services. In other words, companies are not receiving excess purchase orders to justify hiring new employees, or investing in sunk costs. I've met with over fifty companies this year, and their main issue is slack demand.

The current low interest rate environment has resuscitated borderline distressed companies and has given breathing room to firms with high costs of capital. What does this mean? Low interest rates have INCREASED earnings for companies, INCREASED valuations and has DECREASED credit risk for companies. Why do you think there's been a huge influx of capital into junk bonds...?

What the US economy needs is an INJECTION of long term investments, i.e. infrastructure and sunk costs like R&D, non-profit activities, etc. The government can raise the necessary capital by pricing bonds at a spread above the current 30 treasury bond. The government can also offer LOW taxes on capital appreciation of the bond (maybe 5%). Assuming a 5% coupon, if the government were to raise $4T (directly or indirectly through GSE's), the annual interest expense would be $200B.

The influx of $4T might induce inflation, but that could be controlled by an increase in interest rates. Also, tax revenues would increase via income taxes, capital gains, sales taxes, property taxes, etc.

We can always use numbers to support or debunk a theory, however, economics and life tends to skew towards behavioral variables. Ask Romney!

Based on my direct dealings with lower middle-market enterprises ($50 > enterprise value), the biggest problem affecting incremental increases in capex, is lack of demand. Companies do not need additional goods and services. In other words, companies are not receiving excess purchase orders to justify hiring new employees, or investing in sunk costs. I've met with over fifty companies this year, and their main issue is slack demand.

The current low interest rate environment has resuscitated borderline distressed companies and has given breathing room to firms with high costs of capital. What does this mean? Low interest rates have INCREASED earnings for companies, INCREASED valuations and has DECREASED credit risk for companies. Why do you think there's been a huge influx of capital into junk bonds...?

What the US economy needs is an INJECTION of long term investments, i.e. infrastructure and sunk costs like R&D, non-profit activities, etc. The government can raise the necessary capital by pricing bonds at a spread above the current 30 treasury bond. The government can also offer LOW taxes on capital appreciation of the bond (maybe 5%). Assuming a 5% coupon, if the government were to raise $4T (directly or indirectly through GSE's), the annual interest expense would be $200B.

The influx of $4T might induce inflation, but that could be controlled by an increase in interest rates. Also, tax revenues would increase via income taxes, capital gains, sales taxes, property taxes, etc.

We can always use numbers to support or debunk a theory, however, economics and life tends to skew towards behavioral variables. Ask Romney!

Tuesday, November 6, 2012

Riverside: What M&A Slowdown? - Deal Journal - WSJ

Riverside: What M&A Slowdown? - Deal Journal - WSJ

No one seems to have told Riverside Company that the M&A market is in the dumps...

Interesting details. It appears that buyout companies with a clear strategy, continue to make acquisitions, regardless of the macroeconomic indicators that most investors tend to over-analyze. Targeting $200M > companies can make buyout firms appear acquisitive, but with cost of capital so low (including equity risk premium hovering around 6%), it wouldn't be impossible to have most LBO's with an all in cost of capital of ~5% - 7%.

Assuming a 5 year projected growth rate of 5%, constant or light capex and sticky revenue, the next three years will present tons of opportunities to acquire distressed assets, boring companies (packaged food distributors, etc) or over-inflated companies (when you factor in historic interest rate lows and low cost of equity).

Middle market companies should be wise to accept offers - the helicopter ride will not last for long...

No one seems to have told Riverside Company that the M&A market is in the dumps...

Interesting details. It appears that buyout companies with a clear strategy, continue to make acquisitions, regardless of the macroeconomic indicators that most investors tend to over-analyze. Targeting $200M > companies can make buyout firms appear acquisitive, but with cost of capital so low (including equity risk premium hovering around 6%), it wouldn't be impossible to have most LBO's with an all in cost of capital of ~5% - 7%.

Assuming a 5 year projected growth rate of 5%, constant or light capex and sticky revenue, the next three years will present tons of opportunities to acquire distressed assets, boring companies (packaged food distributors, etc) or over-inflated companies (when you factor in historic interest rate lows and low cost of equity).

Middle market companies should be wise to accept offers - the helicopter ride will not last for long...

Sunday, November 4, 2012

Reading the Fine Print in Abacus and Other Soured Deals - NYTimes.com

Reading the Fine Print in Abacus and Other Soured Deals - NYTimes.com

A common refrain from the financial crisis is that poor disclosure was a big contributor, if not the cause, of the financial crisis. Buyers of even the most complicated financial instruments were misled or were not provided full information concerning their investments. The results were catastrophic when the mortgage market crashed...

I always wonder why Very Serious People hammer Goldman Sachs and friends with their lack of disclosure as a market maker. The last time I checked, market makers buy and sell products/services at approximately "fair value". What does fair value mean?

Fair value means liquidation value at a certain date. Now, if an investor is offered a home to purchase at a $100 price, but a similar house nearby is being offered at $90, what is the fair value of the asset? The fair value is the actual price paid for the asset. Period.

So, why are people mixing market makers with advisers? Advisers are retained to walk in their clients shoes, while market makers make a living by buying AND simultaneously selling assets - to ensure that they are always involved in the trade.

Now, if a sophisticated investor read the Abacus pitch book, invested in the CDO, and lost a substantial amount of capital, who is at fault?

It's time to allow IB's do what they do best, which is market making and advising. Both can lead to sticky conflicts of interest, but hey, caveat emptor...

A common refrain from the financial crisis is that poor disclosure was a big contributor, if not the cause, of the financial crisis. Buyers of even the most complicated financial instruments were misled or were not provided full information concerning their investments. The results were catastrophic when the mortgage market crashed...

I always wonder why Very Serious People hammer Goldman Sachs and friends with their lack of disclosure as a market maker. The last time I checked, market makers buy and sell products/services at approximately "fair value". What does fair value mean?

Fair value means liquidation value at a certain date. Now, if an investor is offered a home to purchase at a $100 price, but a similar house nearby is being offered at $90, what is the fair value of the asset? The fair value is the actual price paid for the asset. Period.

So, why are people mixing market makers with advisers? Advisers are retained to walk in their clients shoes, while market makers make a living by buying AND simultaneously selling assets - to ensure that they are always involved in the trade.

Now, if a sophisticated investor read the Abacus pitch book, invested in the CDO, and lost a substantial amount of capital, who is at fault?

It's time to allow IB's do what they do best, which is market making and advising. Both can lead to sticky conflicts of interest, but hey, caveat emptor...

Hey Big Spender | asymco

Hey Big Spender | asymco

In previous posts I described the patterns of asset value growth for Property Plant and Equipment at Apple and how that change has been thus far correlated to the production of iOS devices....

Apple's PPE is not a good indicator of their capex requirements. Since Apple primarily outsources their tangible capex, I would say that they're a more of a service company vs a hardware company. Last time I checked, their R&D expenses are tiny compared to comparable companies (if you can find a pure play, be my guest).

However, I tend to view capex as a good indicator of growth, and a company's ability to carve out a defensible position within the market. Capex could be increase in employee compensation, training, R&D, patents, etc. No wonder Apple's stock is "undervalued" relative to Amazon: Amazon actually has a defensible business model, even though their profits (or free cash flow) does not indicate that.

In previous posts I described the patterns of asset value growth for Property Plant and Equipment at Apple and how that change has been thus far correlated to the production of iOS devices....

Apple's PPE is not a good indicator of their capex requirements. Since Apple primarily outsources their tangible capex, I would say that they're a more of a service company vs a hardware company. Last time I checked, their R&D expenses are tiny compared to comparable companies (if you can find a pure play, be my guest).

However, I tend to view capex as a good indicator of growth, and a company's ability to carve out a defensible position within the market. Capex could be increase in employee compensation, training, R&D, patents, etc. No wonder Apple's stock is "undervalued" relative to Amazon: Amazon actually has a defensible business model, even though their profits (or free cash flow) does not indicate that.

Subscribe to:

Posts (Atom)